Introduction

Nepal’s income tax system is governed by the Income Tax Act, 2058 (2002) (“ITA”) and Income Tax Rules, 2059 (2003) ("ITR"). The ITA is the primary legislation imposing tax on income from business, employment, investment, and windfall gains. It has been regularly updated by annual Finance Acts, including the latest Finance Act, 2082, to adjust rates and introduce new provisions.

The tax authority, the Inland Revenue Department (IRD), administers the regime under a self-assessment system. All persons with taxable income must register for a Permanent Account Number (PAN) with the concerned Inland Revenue Office under IRD and file annual tax returns.

Nepal follows a uniform fiscal tax year (income year) from mid-July to mid-July (Nepali Fiscal Year). In general, resident taxpayers are taxed on their worldwide income, whereas non-residents are taxed only on income sourced in Nepal. The following sections provide an overview of who is taxed, how individuals and entities are taxed under Nepali law, along with key rates, obligations, incentives, and recent reforms.

Who Is Taxed and On What Basis

Persons Subject to Tax

The ITA taxes “persons”, a term that covers natural persons (individuals) and entities such as companies, trusts, cooperatives, government bodies and other organizations, including foreign permanent establishments (PEs).

Residence vs. Source

Resident persons (individuals and entities) are taxed on their global income, i.e. income derived from any source, inside or outside Nepal. Non-resident persons are taxed only on income having its “source” in Nepal, as defined in Section 67 of the ITA.

Resident Entities and Foreign PEs

- A company is resident if (i) it is incorporated under Nepali law, or (ii) its management is effectively controlled from Nepal in any income year.

- A foreign permanent establishment (branch, site, office, or other fixed place of business of a non-resident in Nepal) is taxed in Nepal on the profits attributable to that PE.

- Controlled foreign entities and foreign PEs are also dealt with under Sections 68 and 69 of the ITA, ensuring that certain offshore structures of Nepali residents are not used to defer or avoid Nepali tax.

Source Principle for Non-Residents

Under Section 67, income, loss, gain and payment are treated as Nepal-source if they arise from, among others:

a. Business or investment carried on in Nepal;

b. Disposal of property situated in Nepal;

c. Payments such as interest, dividends, annuities, retirement payments, royalties and service fees made by a resident person;

d. Services performed in Nepal, where the activities relating to the services are carried out in Nepal.

Taxation of Individuals

Residency and Scope

Under Section 2 of the ITA, a natural person is a resident of Nepal for tax purposes if: (a) their normal abode is in Nepal; (b) they spend 183 days or more in Nepal during any 365-day period of the fiscal year; or (c) they are deputed abroad by the Nepal Government during the year.

Resident individuals are subject to tax on their worldwide income, regardless of where it is earned. Non-resident individuals are taxed only on income accrued or sourced in Nepal. For example, a resident Nepali professional must declare both local and foreign income, whereas a foreigner staying short-term (under 183 days) pays tax only on Nepal-sourced earnings. Dual residence is not recognized; an individual is either resident or non-resident for the whole tax year.

Income Heads for Individuals

Section 5 of the ITA classifies taxable income under three heads:

- Employment income (Section 8): salary, wages, bonuses, allowances, benefits in kind and similar remuneration;

- Business income (Section 7): profits from any profession, vocation, trade, or business carried on by the individual;

- Investment income (Section 9): dividends, interest, royalties, rental income, gains on disposal of investment assets and similar receipts.

Taxable income is the aggregate of net income from employment, business and investment, less any allowable losses and exempt amounts.

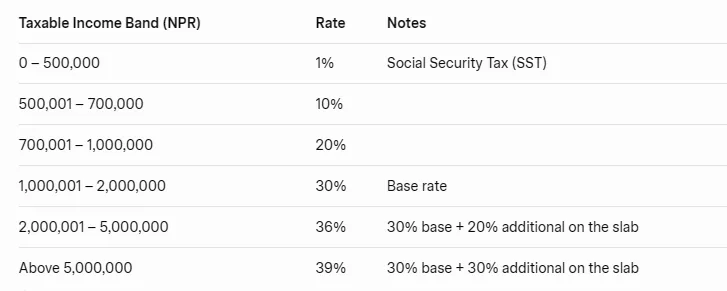

Personal Income Tax Rates (Residents)

Nepal imposes a progressive income tax on individuals. The ITA (Schedule 1) prescribes graduated tax brackets for resident individuals, with a basic exemption threshold of NPR 500,000 for single taxpayers (or NPR 600,000 for married couples filing jointly). Beyond this tax-free band (apart from a nominal social security contribution), the rates increase with income. As of the current fiscal year, the rates for a resident unmarried individual can be summarised as follows:

Married couples can elect for joint taxation, in which case slightly higher thresholds apply for each bracket (e.g. 1% on first NPR 600,000, and so on). These rates and brackets have remained unchanged in recent years. Current Finance Acts should be checked in each year to confirm that the specific slab amounts and any special rebates have not been modified.

Personal Reliefs

Certain reliefs and rebates are available to individual taxpayers:

- The basic exemption for a couple is NPR 600,000 (vs NPR 500,000 for a single).

- A disabled or handicapped individual receives an additional 50% exemption on the basic threshold, meaning an extra NPR 250,000 (single) or NPR 300,000 (couple) of income is tax-free.

- Women taxpayers with only employment income (and not opting for joint filing with a spouse) receive a 10% rebate on their tax liability.

- Senior citizens (age 60 and above) enjoy an additional exemption of NPR 50,000 on their taxable income, effectively raising their tax-free income threshold.

These incentives aim to lessen the tax burden on targeted groups and reflect distributional and social policy objectives.

Non-Residents

A non-resident individual (someone who does not meet the 183-day/abode test) is taxed at a flat rate of 25% on any income earned from employment, business, or investment within Nepal.

The progressive rate slabs and personal reliefs described above generally do not apply to non-residents. For example, a foreign consultant spending 4 months in Nepal will pay 25% tax on their Nepali-source remuneration. However, certain income of non-residents may be subject to final withholding tax at source (discussed later) instead of the 25% rate, depending on the nature of income and applicable tax treaties.

Compliance Obligations (Individuals)

Nepal’s tax year ends in mid-July. Every resident (and non-resident with Nepali income) must file an annual income tax return within 3 months of the fiscal year-end (i.e. by mid-October), unless all their income is already subject to final withholding or exclusively from employment below the threshold.

In fact, an individual whose only source of income is employment salary from a single employer for that income year is exempt from filing a return, subject to the condition that the annual remuneration income does not exceed NPR 4 million, provided the employer has correctly withheld and remitted the tax. Employers report and withhold tax on salaries under a Pay-As-You-Earn system (Section 87 of ITA).

Individuals who must file returns do so under self-assessment, declaring all sources of income and applicable deductions. Failure to file or late filing can attract penalties and interest as described later. All taxpayers are expected to maintain income and expense records; those with business income may need audited financial statements if certain thresholds are met (see Tax Administration below).

Taxation of Companies and Other Entities

Resident and Non-Resident Companies

The ITA imposes income tax on entities, broadly defined to include corporate entities, cooperatives, and certain associations.

A company is considered resident in Nepal if it is either incorporated under Nepali law or if its management is effectively controlled from Nepal during the year. Resident companies are taxed on their worldwide income, while non-resident companies (e.g. foreign companies operating in Nepal through a branch or with Nepal-source income) are taxed only on income sourced in Nepal.

In practice, foreign companies without a legal presence in Nepal may be subject to withholding taxes on payments from Nepal rather than a net income tax (as discussed under withholding).

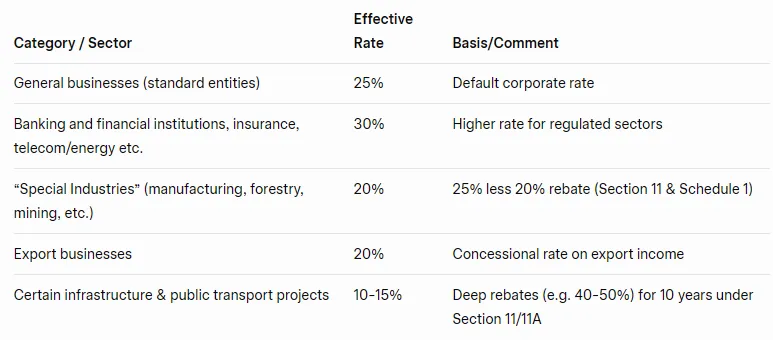

Corporate Tax Rates

The standard corporate income tax rate in Nepal is 25% of net profits for most businesses. However, the applicable rate varies by industry and type of entity, as the law provides differentiated rates and concessions for certain sectors.

Aside from the above, capital gains earned by companies (e.g. from sale of business assets) are generally treated as ordinary income and taxed at the applicable corporate rate. However, capital gains arising from the disposal of investment assets (such as shares, securities, or non-business real estate) are subject to the capital gains tax regime under the ITA and may attract specific withholding obligations.

Dividends paid by a resident company are subject to a final withholding tax of 5% at distribution. This means the company must withhold 5% of any dividend paid to shareholders (resident or non-resident), and that tax satisfies the income tax on the dividend (the recipients do not pay additional tax on it).

Similarly, interest payments, service fees, and royalties paid by companies may attract withholding at various rates (see below).

A non-resident company with a permanent establishment (branch) in Nepal is taxed at the normal corporate rates on its net income attributable to the Nepal operations. Non-resident entities without a branch are typically taxed via withholding on Nepal-sourced payments; notably, income from transporting passengers or goods via sea or air is taxed on a deemed-profit basis - such non-resident transport carriers are subject to only 5% tax on gross fares or freight for shipments embarked in Nepal, or 2% if the journey does not originate in Nepal. These are final taxes in lieu of the general 25% rate on net income for those specific cases.

Section 57 – Change in Control (Entities)

Section 57 of the ITA provides a special rule for change in control of an entity:

- If the ownership of an entity changes by 50% or more compared to its ownership at any time in the previous three years, there is a “change in control” for tax purposes.

- In such a case, the entity is treated, broadly, as if it has disposed of and reacquired its assets and liabilities at market value, potentially triggering tax on unrealised gains.

- After such a change in control, the entity is generally restricted from using certain tax attributes incurred before the change, including: o Carry-forward of interest deduction under Section 14(3); o Carry-forward of prior-year business or investment losses under Section 20; o Certain loss carry-back possibilities.

In practice, this provision is intended as an anti-avoidance rule to prevent loss trafficking and use of shell companies to absorb unrelated profits. At the same time, there has been policy debate about possible double taxation when Section 57 overlaps with capital gains tax on the same transaction.

Tax Incentives, Deductions and Exemptions

Key Exemptions and Sectoral Incentives

Agricultural and Cooperatives Income: Income from agriculture is largely tax-exempt. Section 11(1) stipulates that no tax is levied on income from an agricultural business (whether carried on by an individual or entity) or on other agricultural income from land, subject to conditions. Likewise, income of cooperative societies engaged in agriculture or forest product industries (e.g. farming, horticulture, dairy, beekeeping) is exempt from tax, and even dividends distributed by such cooperatives are tax-free.

Tax Holidays

Beyond the ITA’s built-in rebates, Nepal offers full or partial tax holidays under sector or business specific legislation. For example, newly established industries in certain underdeveloped regions have been granted a 100% income tax exemption for the first 10 years of operation, and hydropower projects that begin commercial generation by a specified date enjoy a full tax holiday for 10 years plus 50% exemption for the subsequent 5 years. Businesses operating in government-designated Special Economic Zones (SEZs) likewise benefit from tax holidays (commonly, 100% exemption for an initial period such as 5 years, followed by 50% exemption for a subsequent period) as provided in the Special Economic Zone Act, 2016.

Other Exempt Amounts

Certain specific incomes are exempt or taxed favourably. For instance, in some cases, a Nepali citizen’s foreign-source income from employment or pensions with foreign governments may be exempt in Nepal. Amounts received as life insurance pay-outs or from approved retirement funds can be tax-exempt or taxed at reduced rates. Windfall gains (like lottery or contest prizes) are taxed separately at a flat rate (typically 25%) and not included in regular income. Section 54 of the ITA shields some inter-company dividends from double taxation: dividends paid by one resident company to another resident company that owns 25% or more of the payer’s shares are exempt from tax, to prevent multiple layers of tax in corporate groups.

Allowable Deductions and Expenses

In addition to exemptions, an important component of the tax regime is what is deductible in computing business or investment income. Key provisions include:

General deduction (Section 13): Expenses wholly and exclusively incurred in earning income from business or investment are deductible unless specifically disallowed. This includes normal operating expenses such as salaries, rent, utilities, administrative costs, etc.

Interest deduction (Section 14): Interest paid on borrowings used for income-earning purposes is deductible, subject to limits (including restrictions on interest paid to controlling or related persons and thin-capitalisation-type rules).

Cost of stock-in-trade (Section 15): The cost of trading stock is deductible, following accepted inventory valuation principles.

Repair and maintenance (Section 16): Expenditure on repair and maintenance of depreciable assets is deductible (subject to capital vs revenue distinction).

Pollution control (Section 17): Certain capital and revenue expenditures on pollution control qualify for enhanced deductions.

Research and development (Section 18): Eligible R&D expenses incurred for business purposes are deductible.

Depreciation (Section 19 and Schedule 2): Capital expenditure on depreciable assets is allowed as depreciation on a pooling basis at rates specified in Schedule 2 (different pools for buildings, plant and machinery, vehicles, etc.).

Donations and contributions (Sections 12, 12A, 12B): Donations to approved charities, heritage conservation, sports development and recognised disaster relief/reconstruction funds are deductible within specified limits.

Employment-related incentives (Section 19A): Certain special expenses for providing employment (e.g. for targeted groups or regions) may be deductible or receive enhanced deduction.

Non-deductible expenses (Section 21): Some costs are expressly disallowed, such as personal/domestic expenses, income tax itself, penalties and fines, and certain provisions that are not yet realised losses.

Overall, the incentive architecture is a mix of (i) lower tax rates for priority sectors, (ii) full or partial exemptions, and (iii) generous deductions and accelerated allowances for particular types of expenditure.

Accounting Basis: Cash and Accrual

The ITA recognises two principal methods of tax accounting:

- Accrual basis (Sections 22 and 24): The default for most businesses and entities. Income is recognised when it is derived (earned) and expenses when they are incurred, regardless of when cash is received or paid. Medium and large taxpayers and companies are generally required to use accrual.

- Cash basis (Section 23): Smaller taxpayers or certain specified persons may use the cash basis, recognising income when received and expenses when paid. This is often permitted for individuals or small professional practices whose scale and complexity do not justify full accrual accounting.

The method chosen must be applied consistently, and any change requires permission from the IRD. The accounting basis interacts with the rules on long-term contracts (Section 26) and bad debts (Section 25), which provide further guidance on timing.

Withholding Tax System

Nepal operates a comprehensive withholding tax (WHT) system as a means of tax collection at source. The ITA (Chapter 17) obligates payers of certain income to deduct tax and remit it to the government, which either pre-pays the recipient’s tax or serves as a final tax on that income. Key withholding provisions include:

Employment Income (PAYE)

Under Section 87, every employer in Nepal must withhold income tax from salaries, wages and other remuneration paid to employees. The tax is withheld according to the individual tax brackets (after the personal exemptions) applicable to that employee’s income. Employers are responsible for depositing the tax monthly and providing an annual withholding statement for each employee. This Pay-As-You-Earn system means most employees have their tax obligations settled via employer withholding.

Investment and Other Income

Section 88 requires withholding at the rate of 15% on various payments made by a resident person that are of an investment nature. This includes payments of interest, royalties, payments for the use of natural resources, rents, and payments for services (service fees/consulting) that have a source in Nepal. For example, a company paying royalties to an author or interest to a lender must deduct 15% at source. There are exceptions: interest paid by banks and financial institutions on deposits of individuals is subject to only a 5% final withholding tax (this lower rate encourages personal savings). Similarly, certain retirement payments have 5% or 10% withholding as per rules. The 15% withheld on most investment payments to residents is creditable against the payee’s tax liability, except where specified as a final tax.

Contractual Payments

Section 89 provides that any resident making a payment for contracts or services in excess of NPR 50,000 must withhold 1.5% of the gross amount (commonly known as “TDS on Contracts”). This covers payments to contractors, consultants, and suppliers for work or services. The withheld 1.5% serves as an advance tax for the recipient (usually a business) which can be credited against their eventual tax due. Certain payments like general insurance premiums also fall under this clause.

Dividend and Other Final Withholdings

Dividends distributed by Nepali companies are subject to a 5% withholding, which is a final tax on that income (neither the company nor the recipient owes further tax on the dividend). Likewise, bank deposit interest of individuals is taxed at a final 5% at source, and some other payments to residents (lottery prizes, retirement fund pay-outs, etc.) have specified final WHT rates. For non-residents, most Nepal-sourced payments (e.g. service fees, royalties, interest, commissions) are also subject to withholding tax, generally at 15% (which is typically final for the non-resident). The idea is to capture tax from foreign recipients who may not file returns in Nepal. For example, if a Nepal company pays a foreign consultant USD 10,000, it must withhold 15% (around USD 1,500) and remit that to the IRD; the consultant receives the balance and usually has no further Nepal tax to pay (the 15% is final, absent tax treaty relief). Certain cross-border payments have special rates by law or treaties, as noted, international air/ship operators are subject to 2% or 5% final tax on their gross receipts in lieu of the standard rate.

Finality of Withholding Tax

Under the ITA, some withholding is expressly designated as “final withholding tax” in respect of that income. Where withholding is final:

- The withheld amount fully satisfies the income tax liability on that particular income;

- The income is generally not required to be included in the taxpayer’s annual return; and

- No additional tax, deduction, or refund arises in relation to that income (i.e. losses or expenses cannot be set off against it, and over-withholding is not refunded).

Typical examples of final withholding include:

- 5% WHT on dividends distributed by resident companies;

- 5% WHT on bank deposit interest of individuals;

- 25% WHT on windfall gains such as lottery or prize winnings;

- 2% or 5% WHT on gross receipts of non-resident air/ship operators; and

In contrast, other withholding (e.g. the 1.5% contract TDS, or 15% on many investment payments to residents) serves as advance tax and is creditable, not final. In those cases, the underlying income must be declared in the return, and the tax withheld is set off against the final assessment.

For non-residents, where WHT on Nepal-source income is final, this often removes the need for the non-resident to file an income tax return in Nepal in respect of that income, unless they have other Nepal-source income not covered by final WHT or a permanent establishment in Nepal.

Double Taxation Avoidance Agreements & Foreign Tax Credit

Tax Credit

Nepal’s tax law provides a foreign tax credit to resident taxpayers for taxes paid abroad on foreign income, up to the amount of Nepal tax applicable to that income. This prevents double taxation for Nepali residents with overseas income.

Double Taxation Avoidance Agreements & Foreign

Nepal has entered into a number of Double Taxation Avoidance Agreements (DTAAs) with foreign states. Section 73 of the ITA empowers the Government of Nepal to conclude such agreements, and where a DTAA applies, its provisions can override domestic law to the extent of inconsistency.

Nepal has entered into a number of Double Taxation Avoidance Agreements

Nepal has entered into a number of Double Taxation Avoidance Agreements (DTAAs) with foreign states. Section 73 of the ITA empowers the Government of Nepal to conclude such agreements, and where a DTAA applies, its provisions can override domestic law to the extent of inconsistency.

As of recent public records, Nepal has signed DTAAs with

As of recent public records, Nepal has signed DTAAs with (among others) India, China, Sri Lanka, Pakistan, South Korea, Thailand, Mauritius1, Austria, Norway, Qatar and Bangladesh. These treaties: (a) Allocate taxing rights between Nepal (source state) and the other country (residence state); (b) Provide for reduced WHT rates on cross-border dividends, interest and royalties; (c) Set out common rules for permanent establishment; (d) Cover capital gains, employment income, pensions, directors’ fees and other income; and (e) Include non-discrimination, mutual agreement procedure (MAP) and exchange of information articles.

Treaty Benefits in Practice

For a non-resident entitled to treaty protection, WHT on dividends, interest or royalties may be reduced below domestic rates, provided the payee is the beneficial owner and supplies a tax residency certificate and other required documentation. Nepali residents receiving income from a treaty partner state can also rely on the treaty to avoid double taxation and then use Section 71 (foreign tax adjustment) for any remaining foreign tax.

Foreign Tax Credit

A resident person may claim a credit (adjustment) in Nepal for foreign income tax paid on assessable foreign income. The credit is typically limited to the Nepali tax payable on that foreign income; any excess foreign tax is not refundable but may sometimes be carried forward as per detailed rules or taken as a deduction instead of a credit. Separate calculations may be required by country and by income type.

In addition, Nepal has begun updating treaties to include anti-treaty-shopping and anti-abuse provisions, in line with global standards. Recent policy moves have focused on notifying treaty partners about anti-abuse measures, aligning with international efforts to combat tax avoidance.

Tax Administration, Advance Rulings and Compliance

Tax Year and Filing

The Nepali fiscal year (and tax year) runs from Shrawan 1 to Ashad 31 in the Bikram Sambat calendar, roughly July 16 to July 15 in the Gregorian calendar. Tax returns for the year must be filed by the end of Ashwin (around mid-October), i.e. within 3 months of year-end.

Advance Rulings

Taxpayers may seek an advance ruling from the IRD on the tax treatment of a proposed transaction. An advance ruling: (a) provides binding clarification (subject to conditions) on how the ITA will apply to the specific set of facts described; (b) helps reduce uncertainty and tax risk, particularly for complex or cross-border structures; and (c) Must be applied for in writing, with full disclosure of relevant facts.

Payment of Tax

Tax is paid throughout the year via withholding and advance tax instalments. Taxpayers with business or professional income must pay quarterly advance tax based on expected liability (commonly 40%/70%/100% instalments). Any balance tax due (or refund claim) is settled upon filing the final return. The IRD has procedures to refund overpaid tax.

Accounting and Audit

Businesses must maintain accounting records and prepare financial statements. All companies and firms must have their accounts audited annually by a licensed auditor and submit audited financials with their tax return. The audit requirement is waived for small taxpayers with turnover not exceeding NPR 10 million; such taxpayers can self-certify their financial statements.

Administration and Enforcement

The Director General of the IRD oversees tax administration under the ITA. The IRD has powers to assess or reassess tax, request information, conduct audits and investigations, and enforce collection. PAN must be quoted on invoices and tax documents, and non-compliance can lead to penalties. The IRD also issues public circulars (Section 75) and guidelines to clarify law and practice.

Penalties and Dispute Resolution

Withholding violations

If a payer fails to withhold tax when required or does not deposit withheld tax to the government, both payer and recipient can be held jointly liable, and the payer may face additional penalties and, in serious cases, prosecution.

Administrative review and appeal

Taxpayers who disagree with an assessment or penalty have avenues for dispute resolution. Initially, one can file an Administrative Review application to the IRD (typically to the Director General) within 30 days of receiving a tax assessment or penalty notice. The taxpayer must deposit all undisputed tax amounts and 25% of the disputed amount along with the review application. If not satisfied with the administrative review decision, the taxpayer can appeal to the Revenue Tribunal within a further 35 days. To appeal, generally 100% of undisputed and 50% of the disputed tax (including any interest/penalty) must be paid or secured by a bank guarantee. The Tribunal will hear the case and can confirm, reduce, or cancel the assessment. Final appeals on points of law may be taken to the Supreme Court of Nepal after the Tribunal’s decision. This staged deposit requirement is designed to ensure taxpayers have genuine grounds for dispute and to secure the revenue while the dispute is ongoing.

Infrastructure Projects and Change-in-Law Protection

Tax on Construction and Operation of Infrastructure

Where an agreement is concluded between the Government of Nepal and a person for the construction and operation of infrastructure (e.g. hydropower plants, highways, airports or similar projects), Section 11A provides a form of tax stability/change-in-law protection: “…the person constructing and operating such infrastructure shall enjoy the tax facilities provided by the law in force at the time of execution of the agreement for the whole period of the agreement.”

This means that, for the term of the concession or project agreement, subsequent changes in the ITA or Finance Acts that are less favourable should not ordinarily strip away the originally granted tax benefits, subject to the exact terms of the agreement and any specific carve-outs. For investors in infrastructure, this provision is a critical comfort on long-term tax certainty.

Recent Developments and Reforms

Digital Service Tax (DST)

DST at 2% on turnover of foreign digital service providers, with an increased threshold (NPR 3 million) and alignment with VAT registration for non-residents.

Expanded PE definition

Inclusion of digital or electronic presence in the concept of PE, targeting non-residents who earn from Nepal through digital means but lack a traditional physical presence.

New incentives

Extension of benefits and concessional regimes to IT and emerging sectors, alongside existing incentives for tourism, manufacturing and infrastructure.

Administrative modernisation

Greater use of e-filing, online payments, data-matching and third-party information (banks, customs, regulators) to improve compliance and reduce the informal economy.

Conclusion

Nepal’s income tax regime is governed by a comprehensive legal framework that taxes residents on global income and non-residents on Nepal-source income, with distinct rules for individuals, entities and permanent establishments. It combines moderate base rates with targeted incentives, deductions and exemptions, and is increasingly integrated into the international tax architecture through DTAAs and foreign tax credit rules.

While the ITA is detailed and technical in places, its overarching design is accessible when read with IRD guidance and professional advice. For both local and foreign stakeholders, proper planning around residence vs source, choice of entity, PE risk, and available incentives is essential. Investors and taxpayers are strongly advised to seek tailored legal and tax advice and, where appropriate, use tools such as advance rulings to obtain certainty in advance of significant transactions.

Quick Compliance Checklist for Taxpayers (2025)

- Register for PAN if you have taxable income.

- Determine residency status (183-day rule or abode).

- Track all income sources (employment, business, investment).

- Calculate tax using correct slabs; apply reliefs if eligible.

- Withhold & remit TDS on payments (e.g., 1.5% on contracts).

- File return by mid-October; pay advance instalments quarterly.

- Maintain records/audited accounts if required.

- Claim foreign tax credit if applicable; check DTAAs for relief.

- Seek advance ruling for complex deals.

- Review for incentives (e.g., special industries, SEZs).